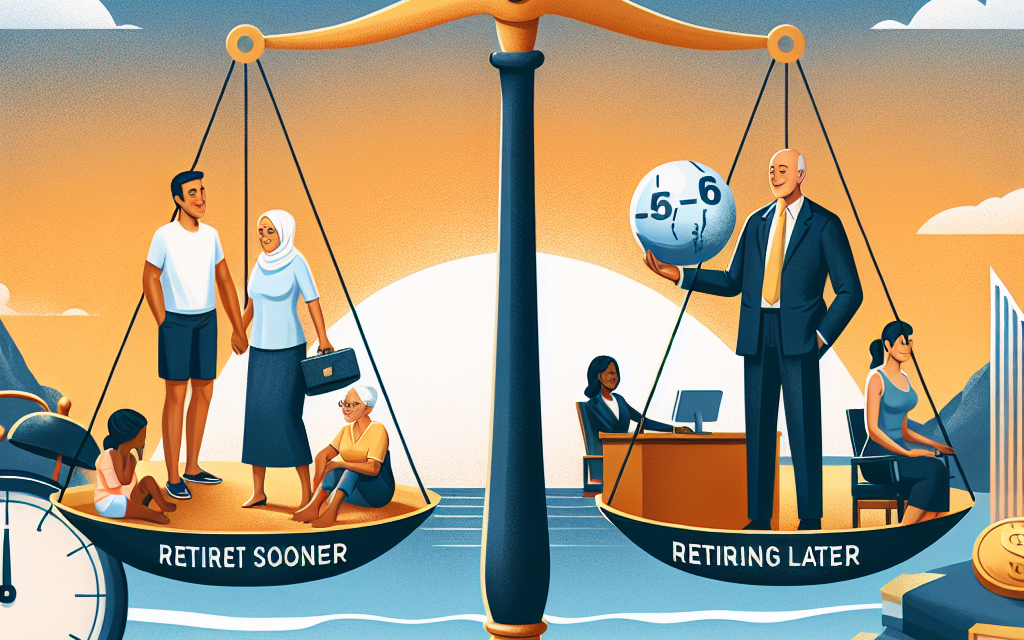

Retirement Planning: Are You Better Off Retiring Sooner or Later?

Retirement is a significant milestone in one’s life, often symbolizing the transition from years of hard work to a period of relaxation, exploration, and personal fulfillment. However, one of the most pressing questions many individuals face is whether to retire sooner or later. The decision is multifaceted, influenced by financial considerations, health, personal goals, and broader societal factors. This article delves into the various aspects of retirement planning to help you determine whether you might be better off retiring sooner or later.

Financial Considerations

-

Savings and Investments:

- Retiring later typically means more years to save and invest, possibly leading to a more substantial retirement nest egg. Compound interest works in your favor, allowing investments to grow over a longer period.

- Conversely, retiring sooner means drawing down on your savings earlier, potentially requiring a more significant initial amount to sustain your lifestyle through your retirement years.

-

Pension and Social Security:

- Pension plans and Social Security benefits often increase with additional years of work. For Social Security in the U.S., for example, delaying benefits from age 62 to 70 can increase your monthly payments considerably.

- If you retire early, you’ll likely receive smaller monthly benefits, impacting your long-term financial health unless you have ample savings to compensate.

-

Healthcare Costs:

- Retiring later typically allows for continued employer-sponsored health insurance. Retiring before becoming eligible for Medicare at age 65 might necessitate purchasing potentially expensive private health insurance.

- Cost of Living:

- The cost of living can vary significantly based on location and lifestyle choices. Retiring sooner might limit travel and leisure activities, whereas retiring later with a larger financial cushion might provide more freedom to pursue such interests.

Health Considerations

-

Physical and Mental Health:

- Your current health and family health history play a crucial role. Those in good health might choose to continue working to maximize their savings, while those with health challenges might prioritize enjoying retirement sooner.

- Mental health is equally important. Job stress and satisfaction levels can dictate one’s readiness for retirement. It might be beneficial to retire sooner if work is causing undue stress or burnout.

- Longevity:

- Actuarial studies suggest that the average lifespan is increasing. Retiring later might be a practical choice for those who anticipate a long and active retirement.

- Conversely, those with shorter life expectancy due to genetic factors or chronic illnesses may wish to retire sooner to maximize the quality of their remaining years.

Personal Goals and Lifestyle Choices

-

Desire for Work-Life Balance:

- Some individuals derive significant personal fulfillment from their careers and may prefer to work as long as possible. Others might have hobbies, travel aspirations, or volunteer interests they wish to pursue in retirement.

- Retiring sooner can provide more time to engage in these activities, while retiring later could mean sacrificing some of these experiences.

-

Family Considerations:

- Family dynamics, such as caring for grandchildren or elderly parents, can influence the decision. Retiring sooner might facilitate more family time, whereas continuing to work could provide financial support for family needs.

- Sense of Purpose:

- Work often provides a sense of identity and purpose. Transitioning to retirement might require finding new ways to stay engaged and fulfilled, whether through part-time work, volunteering, or engaging in social activities.

Broader Societal Factors

-

Economic Climate:

- The economy’s health can influence retirement timing. Economic downturns might deplete savings, encouraging extended employment. Conversely, a robust economy might provide more confidence in retiring sooner.

- Cultural Norms and Policies:

- Different countries and cultures have varying norms and policies regarding retirement age. For example, some countries have higher mandatory retirement ages, which could impact personal choices.

Conclusion

The decision to retire sooner or later is deeply personal and depends on a myriad of factors. Financial stability, health status, personal goals, and broader societal influences all play crucial roles. A comprehensive evaluation of these elements, potentially with the guidance of a financial advisor, can help ensure that you make an informed decision that aligns with your aspirations and circumstances.

Retirement, whenever it begins, should ideally be a period of enjoyment, contentment, and fulfillment. Whether you choose to retire sooner or later, thoughtful planning and consideration can help you achieve the retirement you envision.

{kind=link}